Mark Ritson: Marketers are clueless about media effectiveness – here’s the proof

Radiocentre and ebiquity’s new report forensically lays bare marketers’ perceptions about which channels perform best, and the extent to which they are divorced from reality.

By Mark Ritson

By Mark Ritson

Being sent new research or industry reports is a common experience for columnists. I’ve been writing for Marketing Week for a long time and rarely does a fortnight pass without an approach from an entirely delightful PR person or corporate marketer wanting to share the results of the latest wah-wah about blah-blah arriving at my door.

Being sent new research or industry reports is a common experience for columnists. I’ve been writing for Marketing Week for a long time and rarely does a fortnight pass without an approach from an entirely delightful PR person or corporate marketer wanting to share the results of the latest wah-wah about blah-blah arriving at my door.

I always have a little sniff: who knows what has been uncovered and even if the sample is too small or the method highly incredulous, it always gives you an idea of the current marketing context to see who is researching what.

So, a few weeks ago when a contact from the radio industry told me she had some “research she wanted to send my way” I told her to do just that and promptly forgot all about it until the report, ‘Re-Evaluating Media’, arrived in my inbox.

I opened it. And I am not sure when my mood went from the usual polite suspicion to the state of mind I like to describe as ‘fuck me’, but it happened so fast I was emailing questions to my contact who had sent me the report within five minutes of opening it for the first time.

It’s hard to explain just why this is such an important report. Hard because the world of marketing is so cynical and tribal these days that every piece of research has an almost immediate rejection factor before it has even been viewed. It’s also hard because this report fits with my worldview, which makes it look like that is the reason I love it.

In truth, it’s nice to see empirical evidence of your own hunches but the real value of this new report is the rigour that has gone into it. That, and the simple elegance of what it tells marketers to do as a result of the findings. I have no doubt this will be a signature source of data – quoted and debated for many months to come.

Methodology

Radiocentre – the group charged with promoting the use of radio as a commercial medium in the UK – hired communications consulting firm Ebiquity to review the state of marketing media in 2018. The media examined in the study are the 10 major channels that account for the vast majority of advertising in this country: direct mail, magazines, newspapers, online display, online video, out-of-home, radio, social media and TV.

Media like radio and newspapers are dismissed far too easily by marketers, who need to open their minds to the real possibilities.

Now before I go any further I know what you are thinking: this is just going to show that radio is the best medium for ROI, reach, engagement, everything. Every major channel has knocked out some dodgy research in the past few years with a slightly ropey academic, which claims they generate 14 or 20 times the value of their rivals and you should spend all your budget with us not them.

Well not quite.

After the initial brief, Radiocentre allowed Ebiquity to work on the project without any direction at all. None of the agencies or clients interviewed knew that the research was being conducted on behalf of a radio client. You also have to remember that Ebiquity has to guard its independent status too or lose most of its current, not insignificant, standing in the world of marketing and media.

Most impressively, despite radio paying for this research it does not come out top of the rankings, as you will see as you read on. In fact, of the 13 tables contained in this report comparing the different media, radio makes it to the top of just one of them. That does not sound like fluff or research bias to me.

Ebiquity’s challenge was to compare the perceptions of advertisers and agencies on various advertising media with the reality of what each of these media channels actually offers, according to third-party assessment.

For the perceptions part, Ebiquity interviewed 68 marketers working in companies that spent £2m or more on advertising last year. There are not that many companies spending that much on advertising so this is a big sample.

Ebiquity also interviewed executives from 48 different advertising agencies (covering the gamut of media and creative shops). This must be, by some measure, one of the most robust samples of British advertising people in quite some time.

To assess the actual performance of each channel, the Ebiquity team used secondary data from a wide variety of places. Fifty different sources and more than 75 published reports – all conducted since 2010 – were used to build a picture of how each channel performs against the others.

Ebiquity combined this data with its own proprietary benchmarks from working with a multitude of global clients and linked this information to third-party evidence such as the IPA’s influential touchpoints data. It’s a huge effort and one that provides an up-to-date and highly detailed view of the current British media environment.

The results

Even before we get to the actual performance versus perception data for the various media channels, this data provides a fascinating snapshot of what marketers want from their media in 2018. Participants were asked to rate the importance of the dozen different criteria for media using a MaxDiff trade-off method (identifying the most and least important options from multiple lists), which avoids the usual criticisms of simple verbatim answers or ranking data.

READ MORE: Marketers undervalue the impact of traditional media channels

It is clear that there are four main drivers for media selection in 2018. Marketers are looking for clear targeting cut-through, the ability to show strong ROI, a positive emotional response to the message and increased brand salience at the same time. If you put Byron Sharp, Peter Field, Les Binet and the IPA in a big industrial blender this is probably the juice that the concoction would produce. So, no real surprises.

In contrast, many of the industry’s other obsessions appear to be far less important to marketers. The push for transparent third-party measurement and brand safety might be hot topics for most marketing conferences but they are not on the radar for the average advertiser. Low cost does not appear to be much of an attraction either.

If I could be critical of the sample’s responses just once it would be the relative weak performance of ‘gets your ad noticed’. There is a ton of evidence to suggest that most advertising simply does not even break into the consciousness of the target market and I would have expected marketers to push this issue higher up the agenda.

But the interesting part of the report is examining how marketers think the various media perform against these dozen demands and then looking at what the hard evidence says their actual performance is. For reasons of focus and length I will keep my assessment to the top four main drivers for this column but interested readers are encouraged to download the full report here.

Targeting

It’s perhaps no surprise that direct mail (the legacy medium for micro-targeting) and social media (the digital entrant most famous for its ability to reach very specific audiences on a personal level), feature at the very top of the perception chart for targeting. It has been drummed into every marketer that the personalisation of LinkedIn or Facebook makes for dramatically different marketing opportunities.

It’s perhaps no surprise that direct mail (the legacy medium for micro-targeting) and social media (the digital entrant most famous for its ability to reach very specific audiences on a personal level), feature at the very top of the perception chart for targeting. It has been drummed into every marketer that the personalisation of LinkedIn or Facebook makes for dramatically different marketing opportunities.

And yet, when the data is crunched, at the top of the evidence-based ranking is radio – thanks to its ability to reach consumers by geography, demographics, context, time of day, day of week and even addressability with the new connected listening revolution that is taking place.

It might look like a dubious result – and it is the only category that radio triumphs in – but the big insight is that if you use multiple stations and distinct program context combined with time of day, the ability to slice and dice your audience and reach a tight segment of the market is not only possible but readily advantageous.

You do have to feel for the executives at the Radiocentre and begin to get a glimpse into why they have ploughed so much money into this research. There is radio, top of the performance charts for targeting according to the data, and yet it sits at the bottom of the perception charts, joint-last in the mind of clients. Radio has a marketing problem; that is for sure.

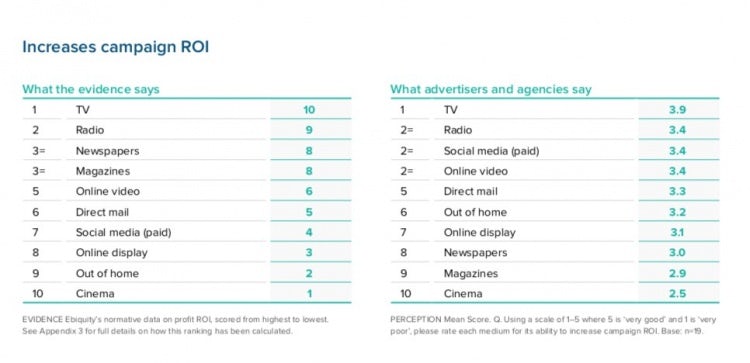

Return on investment

For return on investment (ROI) there is, at least, a much closer correlation between perception and performance. Echoing other research from other independent sources, it is clear that digital media in general gets far too much credit for delivering an ROI versus its actual performance.

In contrast, one again must feel some sympathy for news media, which are perceived as having little to any impact on ROI. In reality, they offer some of the most significant campaign lifts for those clients that can look beyond the bullshit of the ‘death’ of news media and see both the continued potential of print advertising – the campaign of the year so far, KFC’s FCK ad, was a newspaper ad, lest we forget – and the growing potential of premium digital news media ads.

For the team at Thinkbox, there should be genuine celebration that their concerted and extraordinarily data-driven campaign to push the ROI of TV has worked brilliantly. Similarly, the Radiocentre campaigns to push the return on radio advertising appear to have worked. This is not the attribute they need to focus on any more – many other perceptual shortfalls must be corrected.

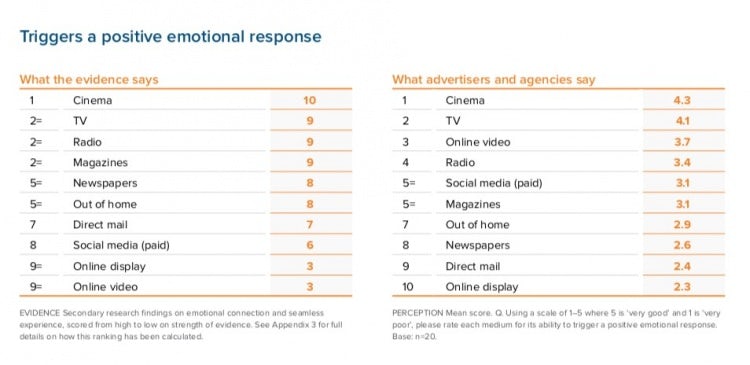

Emotional response

Again, it is impressive to see that marketers are very much aware of the power of both cinema and TV in driving emotional response. As we learn more and more about the longer-range, mass-targeted power of brand-building campaigns, we are also becoming increasingly keen on media that can deliver brand messages with an emotional charge. TV and cinema win out here and the evidence and perceptions of the country’s marketers are aligned.

The interesting disparity comes with online video. Clearly, those investing in the medium believe it vies with the big traditional screens for emotional depth and engagement but, as the ebiquity research shows, the small screen, fleeting attention and often distracting context for consumption lead to it performing dead-last in terms of generating an emotional response.

It’s worth pointing out that all the digital media perform worst on this dimension, meaning that those looking for broad engagement and a more effective advertising impact need to consider investing their money elsewhere.

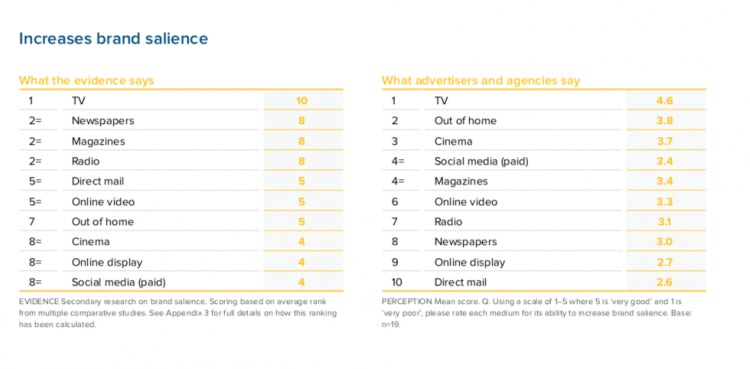

Salience

The concept of brand salience is a fascinating one. It was once a key focus for marketers, then seemed to die away as creative executions and an exaggerated faith in ‘brand love’ led many marketers to believe that their brands were automatically noticed by target consumers.

The reality, as more and more data emerges, is that brands are weak things. Even when consumers can recall an ad the brand behind it is – more often than not – completely ignored. Smart marketers have begun to revisit saliency and ask whether their brand is even noticed before moving on to how it is perceived.

Again we must tip our hat to Thinkbox and the TV companies who have manged to maintain a steadfast claim that TV remains the single best way to get the UK to notice and think about your brand. Again, let us spare a sad few seconds commiserating with news media companies on this issue. The combined data suggest newspaper still set the tone for much of the country and are a great way to propel your brand into the national consciousness, but marketers don’t see it that way.

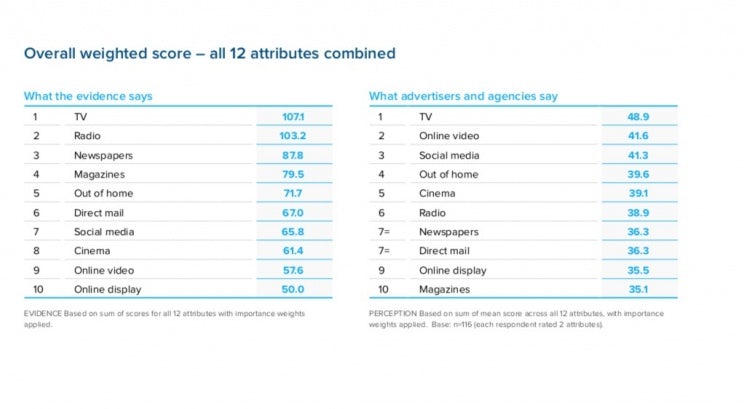

The grand prix

The story continues for the other eight attributes in the ebiquity report. But with all the data compiled and analysed there is one last tantalising league table to show – a grand prix if you will – weighting the 12 attributes to reveal the overall best advertising media.

And here it is. The perceptual table looks very familiar: the idea that TV, online video and social media represent the three leading advertising channels in 2018 would surprise few people. Even the presence of out of home in fourth spot fits with that media’s current renaissance, thanks to the growth in digital screens.

But it’s the evidence-based performance table that should stun marketers. TV retains its dominant position; it’s worth underlining that point given we continue to face dreary marketers getting on stages in their hoodies predicting the end is nigh for TV. But then look at the next top performers according to the actual performance data.

Radio and news media offer significant superiority over social media and online video on the issues that matter most to marketers. And yet radio can only hope for a flat line in terms of advertising spend this year and news media would be happy, I’ll bet, to lose 10% of its share of the advertising pie in 2018.

Meanwhile the digital revolution continues in this country. Marketers and agencies continue to move more and more of their ad spend across to social media and online video despite all the evidence to the contrary.

READ MORE: Unilever increases media spend by £220m and shifts more money to digital

Implications and applications

Here we should pause and apply a major caveat. I continue to believe that there is no superior advertising medium. I believe that it very much depends on your strategy as to which media you should and should not invest in. And when I say strategy I mean four things: the target segment, the strategic objectives, the positioning of your brand and the actual budget you have at your disposal.

Only last week I was arguing strongly against an outdoor campaign in favour of moving money to social media advertising and premium digital display, because my target segment was tiny, my objective was achieving a first appointment, my brand was positioned as a high-end exclusive service, and our budget was more than adequate to get a return there.

Marketers can always justify their media choices and make such a good argument they fool the most critical audience of all – themselves.

My point is that, despite what a bunch of fuckwits from digital agencies might tell you about me, I don’t “hate digital”. I hate it when digital is already being planned and we don’t even have a strategy in place.

I also continue to believe that synergy beats specialism. The idiot marketers (and I insist on the term because I mean it) that continue to push a digital-first approach to media must be shouted down. The power of a good campaign has always been in the combination of different weapons at different stages of the execution to get the job done.

I believe a bit of TV, backed up by radio and then linked to search advertising will deliver a better result than pumping all my money into any one of these options. These Ebiquity league tables show none of these synergies because they treat each media channel, as they must for their analysis, as a separate competing option.

Don’t take that separation into your own brand planning – multiplicity always delivers a bigger outcome than duplication. Diversity beats uniformity hands down. Learn to spread your money accordingly.

But with those two caveats I come back to the same old mantra that has been the boring old bane of my career for the last seven years. I think digital media brings some interesting new options to brand execution but I remain convinced these media are over-sold and over-invested in across most marketing plans.

Media like radio and newspapers are dismissed far too easily by marketers, who need to open their minds to the real possibilities that these fantastic channels can offer. I am not saying spend all, or any, of your money on radio. I am saying if you do not ask your media agency to include radio and news media in your initial consideration you are a fool.

Will it make a difference?

My general admiration for this report and the rigour and sampling behind its findings could not be greater. But now let me remove the happy clown face of empirical respect and reveal the bastard grimace of practical marketing reality. This report is brilliant and it will make not one whit of difference to media spending in the UK, for three insurmountable reasons.

First, a significant number of marketers are not driven by data any more. They look at their own highly unrepresentative media consumption and use that as a proxy for their media planning. The chaos of the last decade of media wars has left many now-senior marketers with the distinct impression that no-one knows which media is best so it’s good enough to go with the flow.

“Sure,” they will say, “those are some interesting tables. But I’ve seen similar from Facebook and Google. We’re good.”

They are also, alas, obsessed with new things and tech. When you suggest print media might be a viable option for their brand they look at you like you have just proposed a deeply offensive sex act. Give me a VR headset with machine learning to go. Newspapers? What planet are you on, grandad? To summarise, they don’t care what the data says.

Second, there is a significant bias within media agencies towards digital media and against so-called traditional alternatives. If you look at the amount of money that can be made in fees and rebates from digital media it is often a factor of three or four times more profitable to recommend digital video over TV or radio.

With those kinds of incentives and the current financial struggles of many advertising groups, there is little if any chance that agencies will lead their clients back to radio or news media in big numbers based on this or any other data. It just does not pay well enough.

Does that mean every agency is putting their own interests before their clients? No. Are many of them doing it? You bet. There’s nothing illegal in pushing your more profitable merchandise, I might add.

But the main reason that this report will fail to have any impact is contained within its very pages. Side by side, we see how the each medium actually performs on various attributes and then next to it the perceptions of marketers and advertisers. Clearly there are big gaps between reality and perception, which need to be removed.

But it turns out that perception creates the reality for most marketers. If you have the word ‘digital’ in your job title you automatically bend reality to ensure that all things technological end up looking better than those things that are ‘traditional’.

If, like most British marketers, you are now committing more than half your marketing budget to digital tactics, it is very hard to step back and acknowledge you might have made an error. Instead, your behaviour drives your perception which structures your reality. The table on the right – perceptions – is far more important than the one on the left – reality.

The psychologist Jonathan Haidt claims that the conscious brain thinks it is in the Oval Office in charge of all the decisions when, in reality, it is actually the press office just rationalising those decisions long after they have been pre-consciously made. It’s a brilliant metaphor, but it also goes a long way to demonstrating the problem with the Ebiquity data.

I have no doubt that the league table scores of the various media are accurate, but the only ranking that matters is the perceptual one next to it. Marketers can always justify their media choices and make such a good argument they fool the most critical audience of all – themselves.

For the few marketers prepared to revise their thinking and take in the ebiquity data, there are genuine competitive advantages to be gleaned from this report. I do not believe that its findings will result in a big swing away from digital options towards radio or news media or magazines. But that is good news for you.

If those media fit your budget, target segments, brand position and objectives then there are bargains to be had out there in media land. Perhaps that is the ultimate implication of this wonderful and confronting report.

Professor Mark Ritson will be teaching the next Marketing Week Mini MBA course from 24 April 2018. To book your place, sign up here.

I just printed this (how old media) and walked it over to the guy who plans our media with our agencies. This is a must read.

Thanks Mark, another great piece on the biases that exist within the industry and the importance of starting with strategy. I’m interested in reading the full report, however doesn’t look like you can download this particular report from the link you shared.

‘What the evidence says’ Brand salience scores derived from a study by Digital Cinema Media which shows that cinema is media that contributes most and magazines generate double that of OOH. I’m not going to spend any more of my morning looking at this. GIGO

But radio is TV’s blind cousin. Sort of ok with reach and segmentation, but none of the charts points out that you won’t be able to show how your product looks like. That is the biggest flaw of the radio.

Mark isn’t suggesting that you should blindly be using radio if it doesn’t suit the strategy for what you’re marketing… Choosing to use radio for a product that doesn’t suit it, or using it as an isolated medium when it should be as part of a broader campaign, doesn’t make sense. In much the same way that blindly thinking you MUST spend most of your campaign budget on digital because “that’s where the kids are” doesn’t make sense.

The crux of this story is that marketers need to stop blindly loving the new shiny thing because it’s new and shiny.

That’s where integration, which Mark talks about, plays a major role. Yes, radio on its own would be a problem for product ads, which is why you would integrate a visual medium into the strategy. Pairing radio advertising with a visual medium would provide much more meaning to people as the radio ad would be backed up by the visual ad.

Think some of the comments above are missing the point. Client and agency perceptions HAVE diverged from the reality.

I missed today’s Radiocentre presentation as I was in a client meeting in which the CPTs of different TV deployments were scrutinized yet YouTube activity at 2p a view had not been, despite that equating to £20 CPT and therefore a considerable multiple to those of TV.

Objective data from respected 3rd parties can help better inform clients and agencies as we navigate the confusing media landscape, so hats off to the media trade bodies that are championing the cause of more evidence based decision making.

Excellent piece, Mark. Thanks for laying out your perspective so thoroughly. Some of it may go over some heads this morning. Perhaps they should take a serious look your Mini MBA course only if they could get bytheir sense of self-importance.

Hmm, this study is full of holes – the scoring system used (in the Appendix) was clearly evaluated by a bunch of people who dont know anything about platform capability – OL Display for example CAN be Geo/demographically targeted and bout contextually (scored as a 1 in the report, not a 2) and Social CAN be day parted if you were so inclined (also Scored as a 1, not a 2) – also, ROI impact studies that are 3 years old are referenced with some others dating back to 2012 – how about using more up to date, modern studies to give this a fresh perspective based on the media and more importantly, consumer climate in 2018? Also, as Ebiquity dont isolate other integrated activity from their TV ROI effectively (as a client, i know this is an issue), i would suggest that the TV ROI figure isnt clean either.

This isnt a true reflection of reality – i get the sentiment that perceptions have diverged and that much is true, but the evidence presented in this report is weak and very misdirected.

Agreed.

Mark – Only 3 comments.

1. Fantastic, really. Thanks for publishing it and making me aware of the full research

2. Not only marketers but an entire cadre of pseudo-experts that go around with titles such as “social media guru”

3. The research does really ignore the effect of creative and the message, which surely has got to be the most important factor.

Interesting point regarding the exclusion of creative, you would think that a well-designed OOH ad would deliver a better relative ROI than a poorly-designed newspaper ad, yet newspaper sits third in this table and OOH way down in ninth. Then again it’s all relative, creative design is only one piece of the puzzle; it would be worth finding out if the secondary sources provided results from content on a level playing field regarding their quality of design.

A real belter Mark. Have shared internally and will explore radio creative. Thanks.

Great read and lovely perspective! Few questions about the data but bottom line each channel has it’s power and optimal use relevant to strategy.

Truth and Worth are rarely definitive

The Radio Centre and Ebiquity report on the true worth of media for brand advertisers finds Radio towards the top of the Worth pile. But dig a little deeper and there are some indicators that ask us to question the nature of ‘Truth’. Channel preferences evaluated using MaxDiff analysis have created a certainty that Advertisers and Agencies value an ‘emotional response’ 4X more highly than having their ‘ad noticed at all’? Or that they value 20X more ‘getting in front of the right audience’ than whether the channel they are using guarantees a ‘safe environment for the message’.

As these calculations shape ‘The Truth’ in this report It is worth a moments consideration of whether if the relative importance of these and other preference indicators were not in keeping with your views and recalibrated, what would then be the reported ‘True Worth’ of a channel such as OOH which evidence suggested is the No1 for Cover, No1 for Frequency, No2 for Low cost audience delivery and No. 3 for Gets your ads noticed.

As the final thoughts in the report clarify, perhaps it is ‘Worth’ exploring the ‘Truth’ of your own objectives.

Am I being totally dense or is PPC notably absent? Seems unlikely it was piled in with online display in which case they just didn’t invite it to participate – which feels a bit wrong. Provoking read otherwise, as usual.

Firstly, congratulations to Ebiquity and Radiocentre for compiling such a comprehensive and thought provoking report, and thanks Mark for showcasing it so well. Of course it is possible to quibble with some of the individual scores for different media on certain factors, or with the weighting used across the factors, but the overall scope is really impressive. At Kantar Millward Brown we have comprehensive UK and global multimedia learning about how different channels build brands, some of which was featured in the DCM study referenced in this report. To be fair to the sponsors of this review, we agree that radio’s effectiveness in the UK is likely underrated. Our data shows it is one of the most cost-effective UK media at building brands (especially driving awareness & building brand associations).

However, the most important points in the article are probably those about defining channel choice based on strategy, and on seeking to maximise synergy effects across channels. We have evidence that synergy effects generally account for 25% of overall campaign effectiveness, so campaigns without synergy are massively missing out. Our recent AdReaction: the art of integration report showed that the strongest synergistic effects are usually in combination with TV, so other media really need to resonate with TV whenever it’s on the plan. We also discovered that integration is far from easy. Less than half of all campaigns manage to maintain integration whilst also making the most of each channel, but those that do enjoy a 57% boost to effectiveness. For more (free) information on how best in class brands achieve this, visit: millwardbrown.com/adreaction

Pretty stupid (convenient) to exclude paid search from the analysis as it’s now over 50% of total digital and would make mincemeat of TV ROI numbers without trying. Usual nonsense from old Gitson.